Image source: Getty Images

The time to look at buying shares is when they’re cheap. And Gamma Communications (LSE:GAMA) stock is at a five-year low right now.

The firm’s update from Tuesday (24 March) isn’t strong. But there are reasons to think the future looks much brighter.

Growth(?)

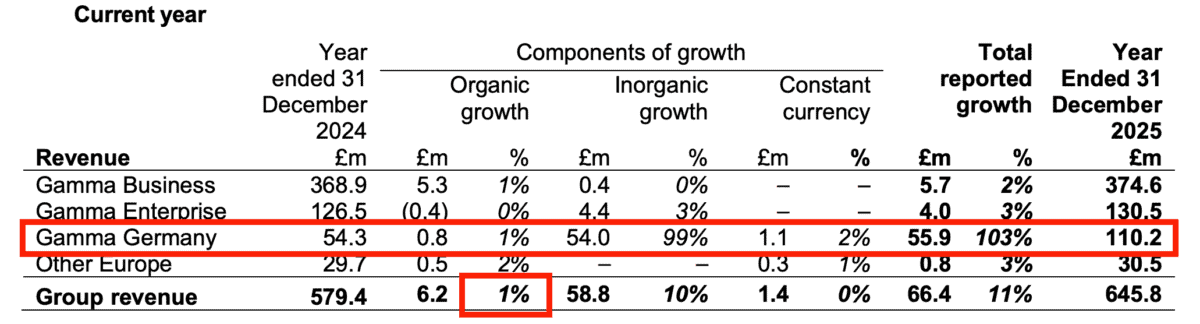

Gamma’s results are complicated. The headline number of 11% revenue growth is strong, but there’s more to it than this.

The majority of the increase is from recent acquisitions in Germany. And this won’t be repeated going forward.

The acquired businesses are doing well, achieving 10% organic growth. But they’re only a small part of the overall company.

Source: Gamma Communications Full Year 2025 RNS

As a result, the most meaningful sales growth number is probably between 2% and 3%. And that’s much lower.

The UK part of the company is facing big challenges. The copper network switch off is weighing on revenues and increasing costs.

That’s why the stock fell 10% after the firm’s results. But while the outlook for 2026 isn’t much better, something big could be on the way.

Up to a point, Lord Copper

The UK switching off its copper phone network at the end of this year is both good and bad for Gamma. But I think it’s more good than bad.

In the short term, it means the end of business line rental and broadband services the firm has provided for years. That’s bad for sales. At the same time, Openreach is increasing line rental prices for remaining customers. That also threatens the firm’s margins.

Eventually, though, companies are going to have to move their phone services to the cloud. And Gamma is the UK leader in this.

The majority of small businesses still need to switch over. That means the potential opportunity ahead is a substantial one. Companies generally don’t change their providers very often. So the benefits of winning new customers could last for decades.

Competition

There’s a big change coming and Gamma could well be set to benefit. But the company won’t have things all its own way.

The big risk is that the firm has to compete with some much larger operators. An obvious one is Microsoft. In terms of competing for cloud customers, Gamma can’t match Microsoft’s scale. But it does have some advantages of its own.

The most obvious is that it’s able to offer better customer support. This comes with having an established network of channel partners. It’s also the result of owning the infrastructure. That means it can offer the ability to intervene to fix problems in ways that Microsoft can’t.

For small businesses that rely on phone numbers working, this could be hugely important. And that’s why the switch is an opportunity for Gamma.

Time to buy?

The stock is at a five-year low and trading at a price-to-earnings (P/E) ratio of eight. That’s also unusually low for the company.

As a result, £1,000 is enough to buy 128 shares. And that’s what I’m planning to do when I’m next in a position to invest.

Analysts aren’t expecting anything in the way of growth for 2026. But they’re more optimistic further ahead.

That fits with the way I see things unfolding for the company. And that’s why I see the lower share price as an opportunity to consider.