Image source: Getty Images

ISA millionaires love dividend shares. That’s a clear takeaway from research on these elite investors from Hargreaves Lansdown and AJ Bell.

Interested to know which dividend shares they like in particular? Here’s a look at the top individual stock holdings of AJ Bell’s ISA millionaires.

Millionaires like blue-chip dividend stocks

Back in February, the broker published a list of the most owned investments among this cohort of investors on its platform. Not only did it highlight their favourite stocks, but it also listed their favourite investment trusts, funds, and ETFs (these people tend to take a diversified approach to investing).

On the stock side, the five most popular shares were:

- Shell

- GSK

- Legal & General

- National Grid (LSE: NG.)

- Aviva

These are all ‘blue-chip’ FTSE 100 companies with healthy dividend yields (ranging from 3%–9%). So, these investors seem to prioritise stability and income.

I should point out though that these aren’t necessarily the best shares to consider buying if someone is aiming to become an ISA millionaire. Most existing millionaires are older investors (many are in their 70s) and an approach focused on stability and income is going to match their goals and risk tolerance.

Someone younger targeting a million-pound ISA could be better off focusing on stocks with more growth potential. This approach could enable them to achieve their goals faster.

Another thing to point out is that the millionaires may have bought these shares for their ISAs 20 or 30 years ago. A lot has changed since then and there could be better opportunities for those investing for the next 10, 20, or 30 years.

A stock for the next 10 years?

Zooming in on the five names though, the one that looks most interesting to me today, from a long-term perspective, is utility powerhouse National Grid. I see it as the most resilient to change and technological disruption (the insurers could face some challenges here).

As the world becomes more digital in the years ahead, demand for electricity is likely to rise significantly (due to the huge power demands of data centres and AI). This is where National Grid comes in – it’s essentially the ‘landlord’ of the infrastructure that makes these technologies possible in the UK (and some parts of the US), pocketing a return on the electricity that flows through its network.

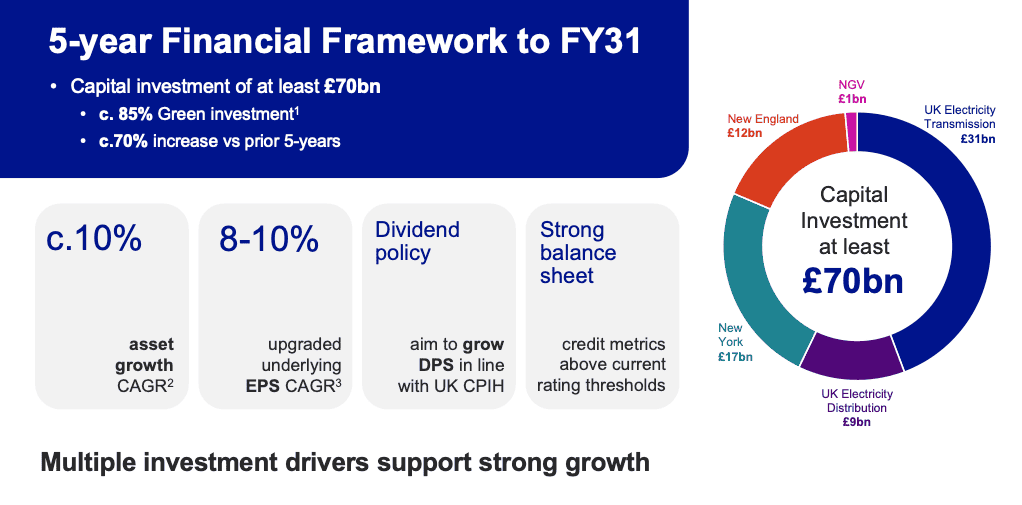

It’s worth noting that the company is spending heavily right now to build out and enhance its network infrastructure for the AI era – between now and FY2031 it plans to spend about £70bn. This kind of spending is a risk as it could hurt profitability.

However, the group believes that it will still be able to achieve underlying earnings per share growth of 8%–10% per year in the medium term (13%–15% this financial year). It’s also planning to grow its dividend payout (where the yield is about 3.6% currently) in line with UK inflation.

So overall, there’s a lot to like, in my view. Trading on a forward-looking price-to-earnings (P/E) ratio of 15, I think it’s worth a closer look today.