Image source: Getty Images

Lloyds (LSE:LLOY) shares are surging more than 8% on Wednesday 8 April.

The index is up too, but this still makes it one of the FTSE 100‘s biggest gainers. Unsurprisingly, it’s the ceasefire agreement between Iran and the US that’s doing the heavy lifting.

Let’s take a closer look and explore whether the stock is worth considering.

War isn’t good for banks

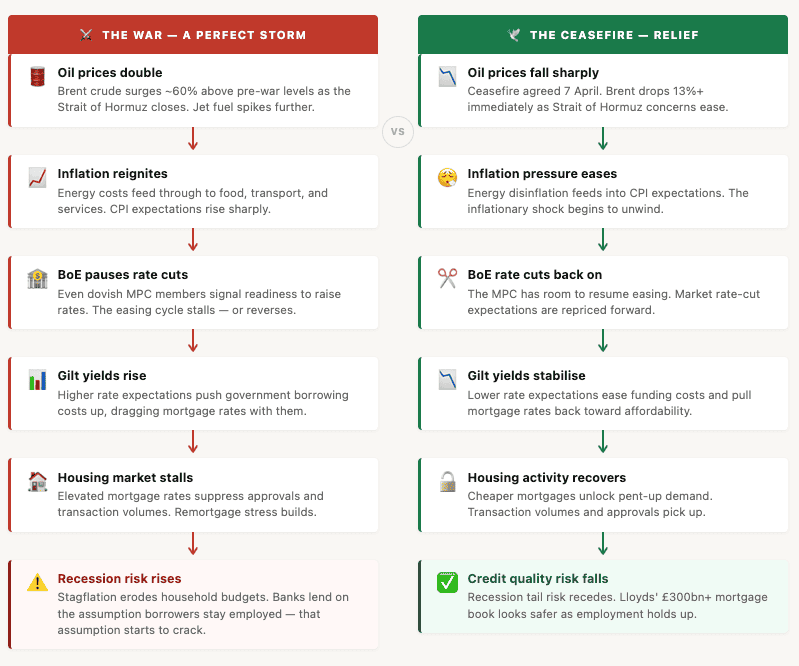

Lloyds is the UK’s largest mortgage lender — it’s really not diversified. That makes it one of the most economically sensitive stocks on the index, and the Iran-US conflict constructed almost the worst possible backdrop for a UK retail bank.

How does this work? Well, the mechanism is like a chain reaction.

War in the Gulf caused oil prices to double — jet fuel went even higher. The spike reignited inflation concerns. In turn, even the most dovish members of the Bank of England’s Monetary Policy Commission were talking about being ready to raise interest rates.

We’ve seen gilt yields rise, mortgage rates stay elevated, and transaction volumes stall. In the long run, sustain high energy prices raised the spectre of recession

However, more worryingly, sustained high energy prices raised the spectre of recession. And recession is the one thing a bank concentrated in UK residential mortgages cannot afford.

There are several reasons for this. But largely it’s because banks lend on the assumption that borrowers will remain employed. A period of energy-driven stagflation quietly erodes that assumption across an entire loan book.

The ceasefire changes the calculus — more so if it holds.

Oil prices have already fallen sharply on the news. If the agreement holds, the Bank of England has room to cut interest rates, consumer confidence can stabilise, and the near-term tail risk to Lloyds’ credit quality falls.

It’s not cheap anymore

Adjusting for today’s 8% gain, Lloyds now trades on a forward price-to-earnings ratio of around 10 times, a price-to-book of roughly 1.28 times, and a forward dividend yield of approximately 4.3%.

Institutional analysts are still pointing to a modest undervaluation, and I think ‘modest’ is the operative word here. It’s trading above book value and, for a purely UK-focused, cyclical retail bank with no investment banking ops, it’s fair, rather than a bargain price.

AI is a risk

The market has been distracted by the war in the Gulf. But before that, back in February, investors were getting worried about AI.

AI is great for productivity, but it may be so great that it leads to a sustained wave of professional job losses that flows directly into mortgage arrears. Lloyds’ £300bn-plus home loan book has more exposure to that scenario than almost any other UK-listed company.

The bottom line

Lloyds shares are not expensive, and the ceasefire — if made permanent — removes a genuine risk. However, with the stock now nudging the higher end of what you’d comfortably pay for a cyclical bank, there may be better value elsewhere.

It’s still worth considering for the long run, but this margin of safety concern should be front of mind.