Image source: Getty Images

Successfully identifying value shares is fundamental to profitable investing. But where to start? Most analysts look at future cash flow forecasts to come up with a valuation in today’s money. This is, however, very labour-intensive. And what if you haven’t got the time to perform these sorts of calculations?

Fortunately, there’s a relatively quick way to try and identify cheap shares. And I’ve used it to find one example of what I believe is a bargain-basement value stock.

A quick overview

As its name suggests, the price-to-earnings (P/E) ratio measures a company’s share price relative to its profit. In simple terms, it defines how much investors are prepared to pay for £1 of earnings. In theory, the lower the number, the cheaper the shares.

However, it’s important to apply a bit of judgement when using the P/E ratio. A low figure could imply that investors are concerned about the company’s prospects. For example, earnings might be going in the wrong direction. And ratios will vary across different industries. Capital-intensive sectors tend to have lower valuation multiples.

Out of fashion

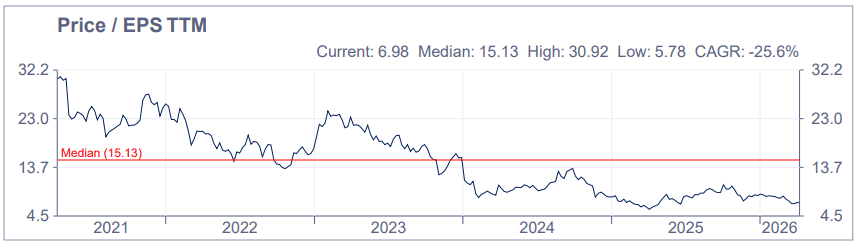

But I think it makes sense to track a stock’s P/E ratio over time. And that’s what makes me think that shares of JD Sports Fashion (LSE:JD.) offer tremendous value at the moment (9 April).

Based on forecast earnings per share (EPS) of 11.37p for the year ended 31 January 2026 (FY26), the stock’s trading on an extremely attractive 6.5 times earnings. The five-year average (median) is 15.1.

And if analysts’ forecasts prove to be accurate, the sports retailer’s forward P/E ratios are 6.5 (FY27) and 5.9 (FY28).

A challenging market

But remember what I said earlier about a low number being a possible warning sign? Well, it could apply here.

The group’s been growing by buying new stores but its like-for-like (LFL) sales have been falling. During the 48 weeks to 3 January, they were down 2.1% compared to the same period a year earlier. The worst-performing region was the UK with a reported 4% drop.

It’s estimated that Nike’s products account for around half of JD Sports’ sales. But the American sportswear giant’s been struggling lately. There are some early signs that it’s recovering but it’s still not out of the woods.

In addition, concerns have been raised that the British retailer’s core demographic of 18-to-24-year-olds are seeing their living standards affected by artificial intelligence solutions replacing entry-level jobs.

Not all bad

Despite these challenges, I still think the group’s shares are in bargain territory.

Over 60% of the group’s stores are now in North America, which are performing better than its European ones. Also, it’s not totally reliant on Nike. Other brands, Adidas being the most notable one, are doing very well at the moment. This year’s football World Cup could also lift sales.

And JD Sports remains cash generative. With free cash flow of over £400m in FY26, it should have the scope to refresh some of its stores in an attempt to get its LFL sales growing again. The consensus of those analysts that have modelled the group’s cash flow potential reckon the stock’s 26% undervalued.

Weighing everything up, I believe JD Sports is well worth considering by investors today.