Image source: Getty Images

Growth stocks are expected to outperform the wider market over the longer term. And their dividends — if they pay them — tend to be lower than average.

Some of these companies are well established and increase their earnings through clever innovation or market dominance. Others might be pre-revenue hoping to find a valuable resource that will change its fortunes forever.

Hot air?

Helium One Global (LSE:HE1) falls into the latter category. It’s started flowing helium to the surface of its mine in Tanzania. This means taking a stake is less speculative than it once was. But it’s yet to sell any gas so buying its shares remains high-risk.

That’s probably why it attracts so much online interest. The prospect of watching an early-stage investment grow into something much bigger is appealing.

Those that invested in, for example, Nvidia, as part of its January 1999 IPO will know what that feels like. But at the time, it was generating profitable sales.

Helium One hasn’t got that far. And that’s why it needs to keep raising money.

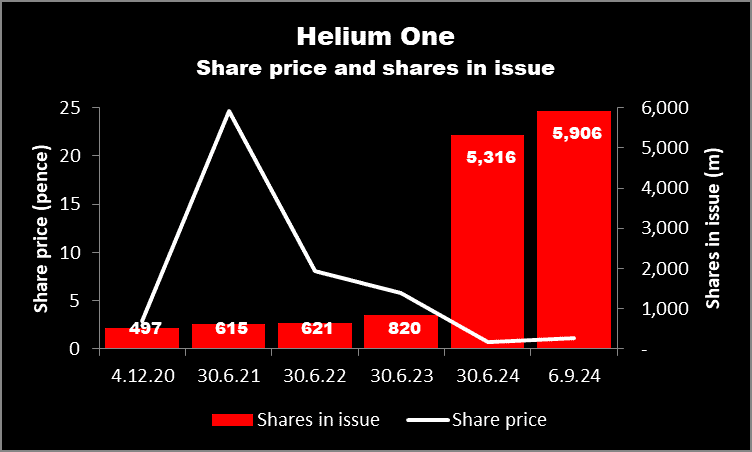

The chart below illustrates that the company now has over 10 times more shares in issue than when it floated in December 2020.

This isn’t a criticism. It’s an inevitable fact of life for a business that’s making losses.

However, it doesn’t appear to have damaged the company’s market cap too much. As the chart below shows, there was an initial peak but it’s still worth over £50m.

Chart by TradingView

But if you were wealthy enough to own 5% of the company at the end of 2020, you’d now have only 0.84%. Of course, this assumes you didn’t participate in any fundraising.

Not for me

And that’s the principal reason why I wouldn’t want to invest at this stage.

To avoid my shareholding being diluted, I think I’d have to part with more cash in the future. However, most of the company’s new shares have historically been placed with institutional investors at a significant discount to the prevailing market price. As a small private investor I probably wouldn’t be able to participate, even if I wanted to.

There are other reasons why I’d be nervous about taking a stake.

Although probably unlikely in Tanzania, there are examples of African governments nationalising companies without any compensation being paid.

Also, from an operational perspective, mining and exploration is one of the most difficult industries. There are numerous things that could go wrong.

However, get it right, and Helium One could be a very lucrative company.

The gas is essential for a number of high-tech applications. Between now and 2030, global demand is anticipated to increase by over 40%.

And according to the company: “The helium market has unique supply, demand and storage dynamics, leading to almost a continual increase in prices.”

But despite these positives, taking a stake would be too risky for me. I’d rather invest in a company that’s selling gas and profitable.