Image source: Getty Images

By mid-afternoon today (20 March), the JD Wetherspoon (LSE:JDW) share price was down around 10% as investors digested the group’s results for the 26 weeks ended 25 January.

The reason? Well, this part of the press release didn’t help:

“There is clearly considerable pressure on consumer finances, combined with higher taxes, wages and energy costs for the hospitality industry. This may result in profits that are slightly below current market expectations.”

But I think the City may have over-reacted. Let me explain.

Easier ways to make money

You don’t have to watch EastEnders to know that running a pub is difficult. However, just imagine the problems that Wetherspoons’ boss, Tim Martin, has to contend with. After all, he has 747 boozers to worry about.

But I love the fact that he’s never shy in explaining the issues that the industry, and his chain in particular, are facing. This morning’s announcement is no different.

With careful reasoning – supported by some insightful numbers — he explained how business rates for Scottish pubs have become a “de facto sales tax”, highlighted the “plethora of stealth taxes (non-domestic electricity charges, climate change levies, packaging charges, etc)” placed on his business, and argued for “VAT equality” with supermarkets.

And this is before we know how the conflict in the Gulf is going to affect disposable incomes and whether the pub chain’s margin might come under pressure from rising costs.

Overall, earnings per share (EPS) for the period fell 32.7% to 18.7p.

Not all bad

But the results did contain some good news.

During the period, like-for-like (LFL) sales increased 4.8% compared to a year earlier. Revenue was also up 5.7%.

In February, industry LFL sales were down 0.2%. For the 42nd consecutive month, Wetherspoons outperformed the wider market with a rise of 3.2%. Sales per pub increased 35.4%.

And the drop in the group’s share price means its stock is, on paper at least, attractively priced.

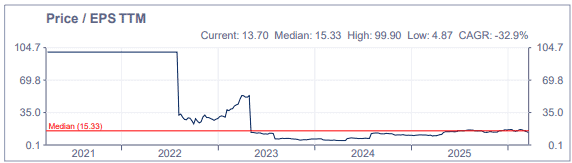

EPS for the year to 25 January was 50.9p, giving a current price-to-earnings ratio of just 10.8. Before today, the five-year average (median) was 15.3.

It’s a similar story when it comes to the group’s balance sheet. Since March 2021, its price-to-book ratio has averaged 2.3. It’s now 1.86.

To be honest, I think today’s 10% drop in the group’s market cap is a little unfair. After all, the group hasn’t said that its full-year profit will be below expectations. It said it “may” be.

So does this mean it’s time to bag a bargain?

Well, it depends. If I knew with a reasonable degree of certainty that the fall in the group’s earnings is a temporary phenomenon then I would say ‘yes’. But given all the problems that Tim Martin lists in his chair’s statement, I can’t be sure.

Based on its revenue, JD Wetherspoon is clearly doing better than the industry as a whole. Pubs are closing all over the place and yet ‘Spoons continues to grow. With its cheap food and drink, prominent high street locations, and strong brand it has lots going for it.

But taking a stake now would be too risky for me. I would like to see an improving bottom line before parting with my money. When I see evidence of this, I shall revisit the investment case.