Image source: Getty Images

Scottish Mortgage Investment Trust (LSE:SMT) shares have been on a monster run. So much so, had someone invested £7,500 in the FTSE 100 growth trust three years ago, they’d now have around £16,500, excluding the low-yield dividend.

The road however, has been far from smooth, with the stock up just 17.5% in five years. This shows how far it fell — 46% in 2022 alone — when interest rates jumped.

To be fair, Scottish Mortgage does warn investors that progress is not linear. Its aim is to invest in outlier growth companies that can deliver multibagger returns over the long run, and these can be notoriously volatile.

[Our] investing style comes with a tolerance for volatility as progress is rarely in a straight line. We are extremely comfortable with the fact that the biggest outliers are often the most volatile.

Scottish Mortgage.

What are outliers?

Companies like Amazon, Nvidia and Apple have compounded at growth rates that dwarf the average annual stock market return. Research shows a relatively small handful of these outliers have accounted for the majority of the market’s total wealth creation.

Therefore, Scottish Mortgage aims to “exploit the asymmetric pay-off structure of equities: uncapped upside yet bounded downside”. In other words, the most that can be lost on a stock is 100% (assuming debt isn’t used), but the potential gains are theoretically uncapped.

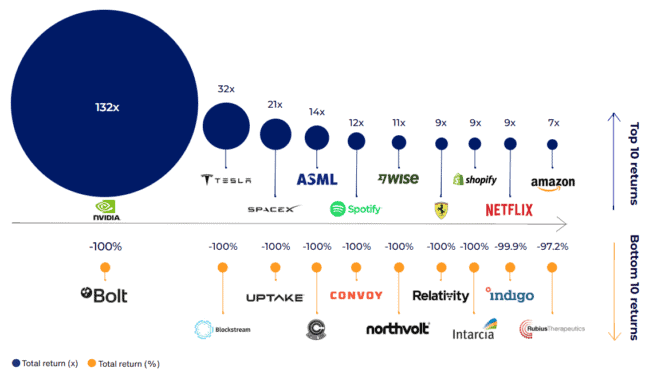

Below, we can see this strategy in action, with a handful of large winners offsetting the losers easily.

Why’s the stock surging?

As we can see, the biggest winners so far have been Nvidia, Tesla, SpaceX, ASML, Spotify, and Wise. The Nvidia holding’s delivered an astonishing 132-fold return!

Note, three of these were private companies when Scottish Mortgage first invested (Spotify, Wise, and SpaceX). And it’s the latter — Elon Musk’s rocket and satellite company — which has really driven the stock up sharply in recent months.

If Musk gets his way, the firm could raise $75bn at a whopping valuation of $1.75trn. As such, the trust has updated its valuation of SpaceX to reflect this potential. It now represents 19.3% of assets.

Still worth a look?

For much of the past three years, Scottish Mortgage has traded at a significant discount to its net asset value (NAV). During this time, many writers here at The Motley Fool have been banging the drum for the discounted stock. So it’s nice to see it flying recently.

However, the NAV discount has turned into a 4.4% premium. And there’s always a risk the discount returns, especially if there’s a tech sector meltdown.

Plus, the portfolio has 14% of assets in China. Personally, I think China carries as much political risk as potential reward. However, many innovative companies are emerging out of the world’s second-largest economy, so it arguably deserves some exposure.

Is Scottish Mortgage still worth considering around 1,420p per share? I think so, assuming an investor has a long-term holding period and is willing to stomach the inevitable ups and downs (and ideally look to add on any significant dips).

Looking ahead, I’m bullish on the portfolio, which holds multiple world-class growth companies that could also go public at huge valuations in the next few years. These include AI lab Anthropic, fintech giants Revolut and Stripe, and TikTok owner ByteDance.