Image source: Getty Images

But first, let me give you some context.

I’ve largely missed the surge in optical networking (the fibre and laser components that carry data between servers inside data centres). Applied Optoelectronics had a monster run — I saw it, shortlisted it, missed a 500% run up in six months.

Lumentum surged after Nvidia put $2bn into it — I owned it but sold too soon. It’s up 800% over six months.

Don’t get me wrong… I’ve done well, but these misses hurt more than losses for me.

I have caught some of the surge indirectly. I own Marvell, which sits at the intersection of custom silicon and optical connectivity. I also have copper cable exposure (typically short-reach within server racks) through Credo.

The really sharp gains have been in the pure-play photonics names.

The great thing about this AI revolution is that the next opportunity is just around the corner. And this got me interested in POET Technologies (NASDAQ:POET).

What is it?

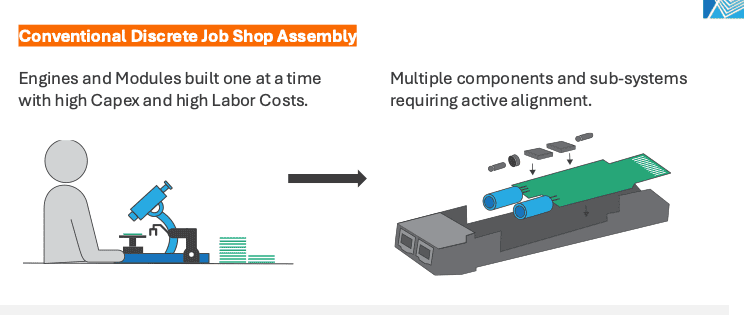

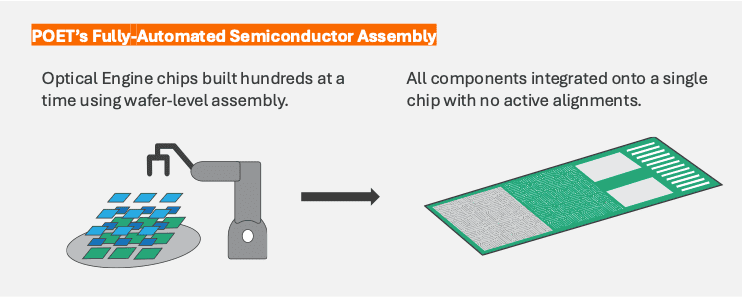

POET isn’t trying to be the new Lumentum. It’s doing something that could be more interesting — rethinking how optical components are assembled in the first place.

Traditional transceivers (modules that send and receive data across fibre networks) stack components with wire bonds, which creates heat, signal loss, and manufacturing complexity.

POET’s optical interposer platform integrates everything onto a single panel. The result is that its Teralight engine reaches 1.6 terabit speeds using just four laser chips, versus the eight or sixteen required by conventional approaches.

There are lots of reasons why this matter.

For one, indium phosphide — the material high-speed lasers depend on — is facing a real global supply crunch. Demand runs at roughly 2m substrates a year; production capacity is around 600,000. Nvidia has already moved to lock up future laser supply from Coherent and Lumentum.

POET’s lower chip count could make it the natural supplier for the tier 2 manufacturers who need to keep building without access to that locked-up supply.

Eyes on commercial signs

The issue is, it’s essentially a pre-revenue company. Revenue projections are for $10m this year and then $80m next year. But it needs to scale even faster to justify the valuation. Investors need to keep their eyes on commercial developments and partnerships.

Currently, the valuation isn’t comfortable. Forward price-to-sales sits around 107 times, against a sector median closer to three times. Market cap is $1.08bn. There’s a cash pile of over $300m and annual burn of around $40m-$50m, which means the company can keep operating for several years without needing to raise more money.

The risk is execution. This story relies on a small number of partnerships hitting their milestones. A slip into 2028 wouldn’t sink the company, but it would hurt the share price badly at these multiples.

The bottom line

POET is genuinely novel technology, in exactly the right place at exactly the right moment in the photonics supply chain. It’s not cheap and it’s not certain. That’s why it’s speculative. It’s worth considering, but the risks are sizeable.